A $90k Salary. A $6.5M Retirement. Here's The Math.

April 7, 2026

People assume that wealth is primarily a function of income. If you earn more, you'll have more! This feels intuitive, but it's mostly wrong.

Meet Alex. Alex graduates college at 22 and starts their professional career with a starting salary of $90,000. This is a very good income, but not exceptional! Alex's income also never becomes exceptional. Over a 43-year career, Alex never earns enough to break into the top 20% of American workers.

Alex retires with $6.5 million.

No inheritance, startup exits, or lucky stock picks. Instead, Alex just has consistent, boring financial habits. Let's talk about what this really looks like.

Meet Alex

From day one, Alex commits to one key habit: 25% of their income goes towards their financial future, as a combination of paying off debt and investing.

Alex also graduated with $30,000 of student loans at a 6.5% interest rate, which is about the average for a bachelor's degree. As a result, their savings will also go towards paying off their loans, not just investing. This means that in year one, Alex sets aside $22,500, of which they put ~$4,000 towards their loan payments and invest ~$18,500. After all of their investments, loan payments, and taxes, Alex has about $4,500 each month to live on. This might be tight depending where Alex lives, but certainly doable.

Alex's salary increases modestly throughout their career, with 5% growth per year through age 35 and just 2% per year after that. After adjusting for inflation, this means Alex's income actually declines after 35. Alex never lands a big promotion, and never gets a big raise from a job hop.

This is deliberate. This model shows the value of this investing system running in the background, even without accounting for significant career growth. This also means that if Alex ever gets a big raise, they can spend that money however they want.

Alex's investments go into a 401(k) first, then a Roth IRA. Their job also never gives them a 401(k) match, which is another conservative assumption. These investments grow at 7% annually in real terms (after adjusting for inflation), which is roughly how a basic index fund performs over the long term.

The Early Years

The early years of Alex's career are the hardest part. Progress feels slow: their investment portfolio is small and they're paying off their student loans. Investment returns also haven't had enough time to contribute much yet.

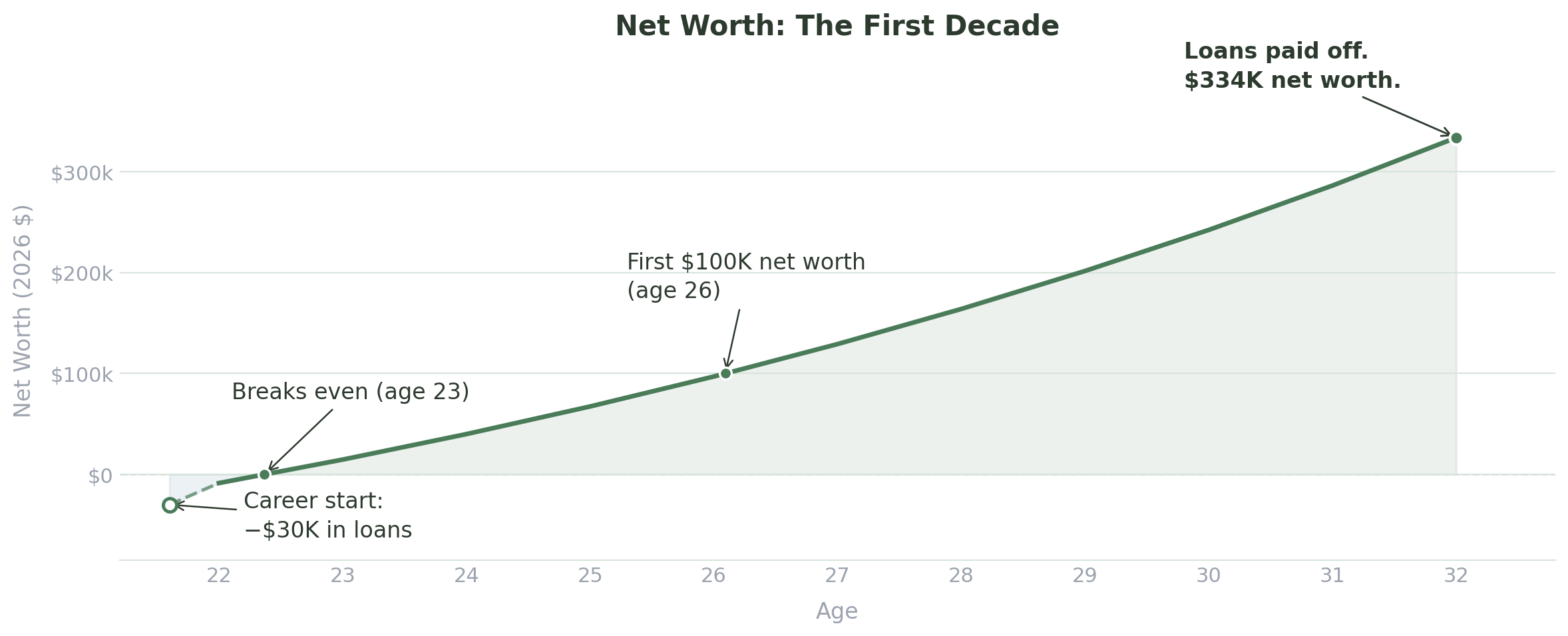

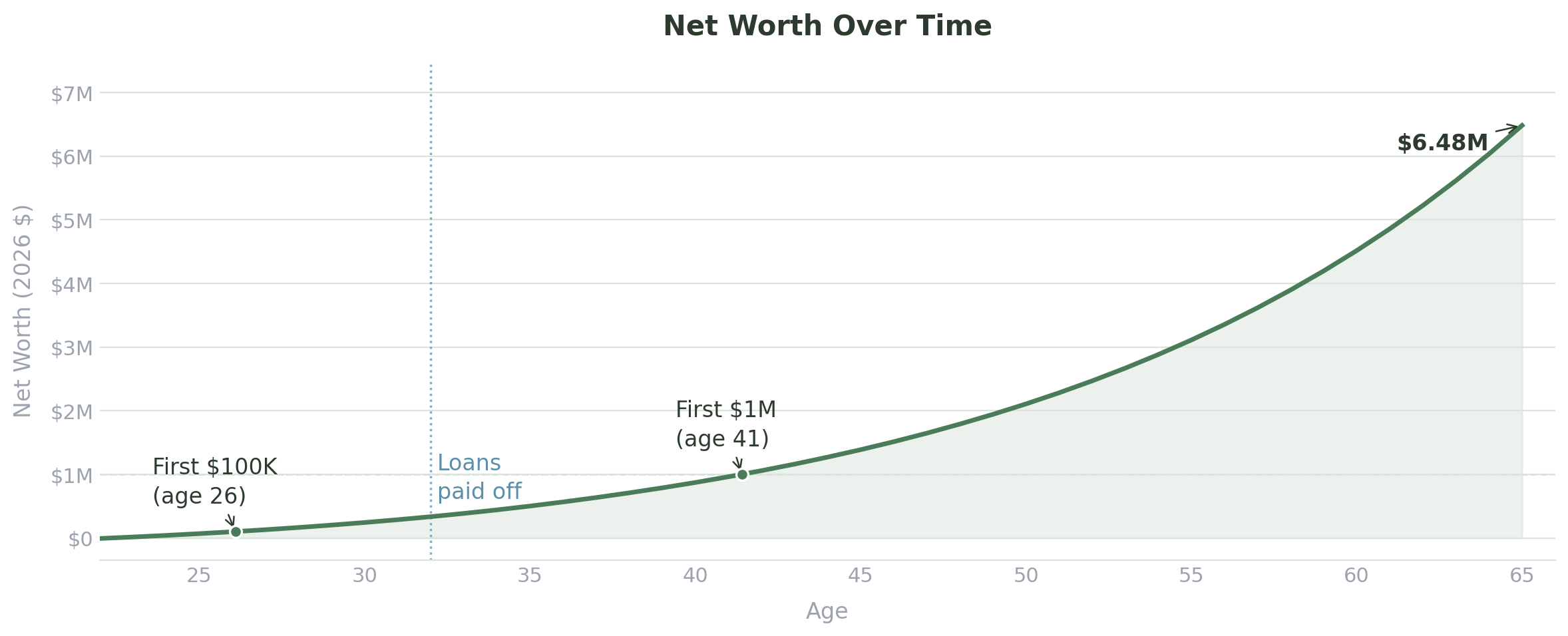

However, Alex is setting up their long-term trajectory very well. There are also great early wins! Alex breaks even on net worth at 23, and hits $100,000 at 26.

Alex finishes paying off student loans at 32 and already has $334,000 in their investment portfolio while never earning a crazy salary or winning the lottery. Now for the first time, Alex can redirect those loan payments to investing more each month.

The hard part of Alex's journey is over.

The Portfolio Takes Over

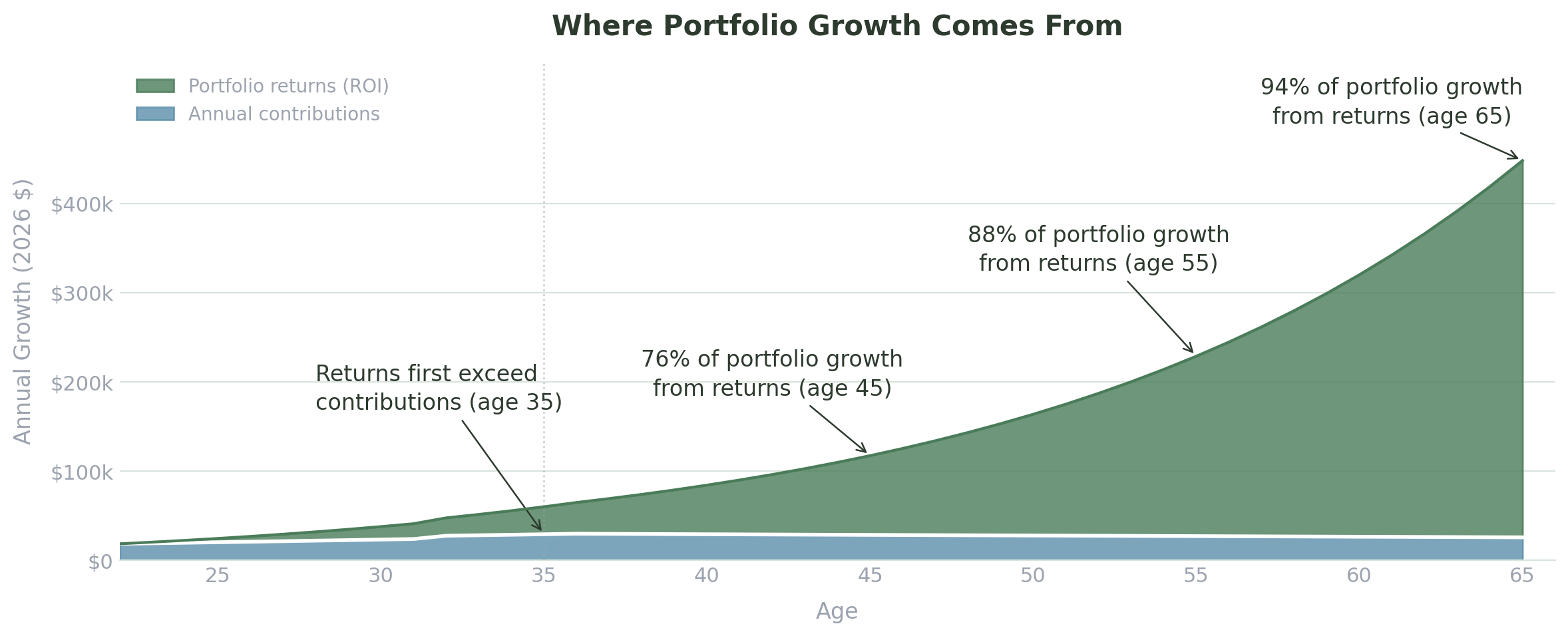

In addition to Alex paying off their student loans, something else is happening: their investment portfolio is large enough that the 7% annual compounding starts to make a visible difference. That $334,000 portfolio generates over $23,000 per year on its own just from sitting in the market.

At 35, the returns from Alex's investments are larger than their annual contributions. The portfolio is hard at work for Alex. By 45, Alex's portfolio is adding over $88,000 per year, which is more than 3 times what Alex is investing. This dynamic gets even more extreme over time, with 94% of Alex's annual portfolio growth coming from investment returns rather than contributions at 65.

In practical terms, this means that Alex actually has much more flexibility in spending well before retirement, as these later contributions barely change their financial trajectory. Alex kept contributions consistent throughout, but honestly didn't even need to. Alex had to work hard to create a solid foundation in their 20s and 30s, but this does most of the heavy lifting by the time Alex reaches middle age. We will come back and explore this concept more in future posts!

The Payoff

At 65, Alex's portfolio is worth $6,480,000 in today's dollars. The culmination of 43 years of consistent, boring habits.

Let's put this in context. Alex's income capped out around $119,000, meaning they never broke into the top 20% of American workers. And yet, by net worth, they retire in the top 3% of American households.

Most people would never expect that someone with Alex's career could have this incredible financial outcome. That's what consistent, boring habits compound into.

A Note on Real Life

Alex's story is intentionally simplified: just one person and a consistent career without major curveballs. Of course, reality is always more complicated.

Alex's lifestyle doesn't increase significantly throughout this trajectory, and this model doesn't account for starting a family, buying a home, or other goals that life tends to introduce.

However, remember that this is also an intentionally conservative career path. Alex never gets a big raise or major promotion, and this doesn't account for a potential partner who could both decrease costs and add income. Every extra dollar is completely free to spend, and the investments just run in the background.

It's also worth noting that Alex's portfolio reaches $2,000,000 at 50. This is a ton of money, and Alex's mindset has already shifted from "am I investing enough" to "what do I want to do with all of this money?" Or perhaps more broadly, "what do I want my life to actually look like?"

Want to run some of your own numbers? Feel free to use my investment return calculator.

Alex's story is just one version. Many people are working with more debt, a later start, or a higher income ceiling. The next post models out a physician trajectory for this.

And if you want to build a financial plan that reflects the life trajectory you want, that's what my 1:1 coaching program is for. Feel free to reach out and set up a free consultation.

Get notified when new posts go live.