From $250K in Debt to $7.5M: The Doctor Trajectory

May 5, 2026

Most doctors watch their student loan balance frustratingly grow throughout residency, as interest dwarfs their payments. While many people assume that doctors are guaranteed to be wealthy, large loan balances have a significant impact both financially and emotionally.

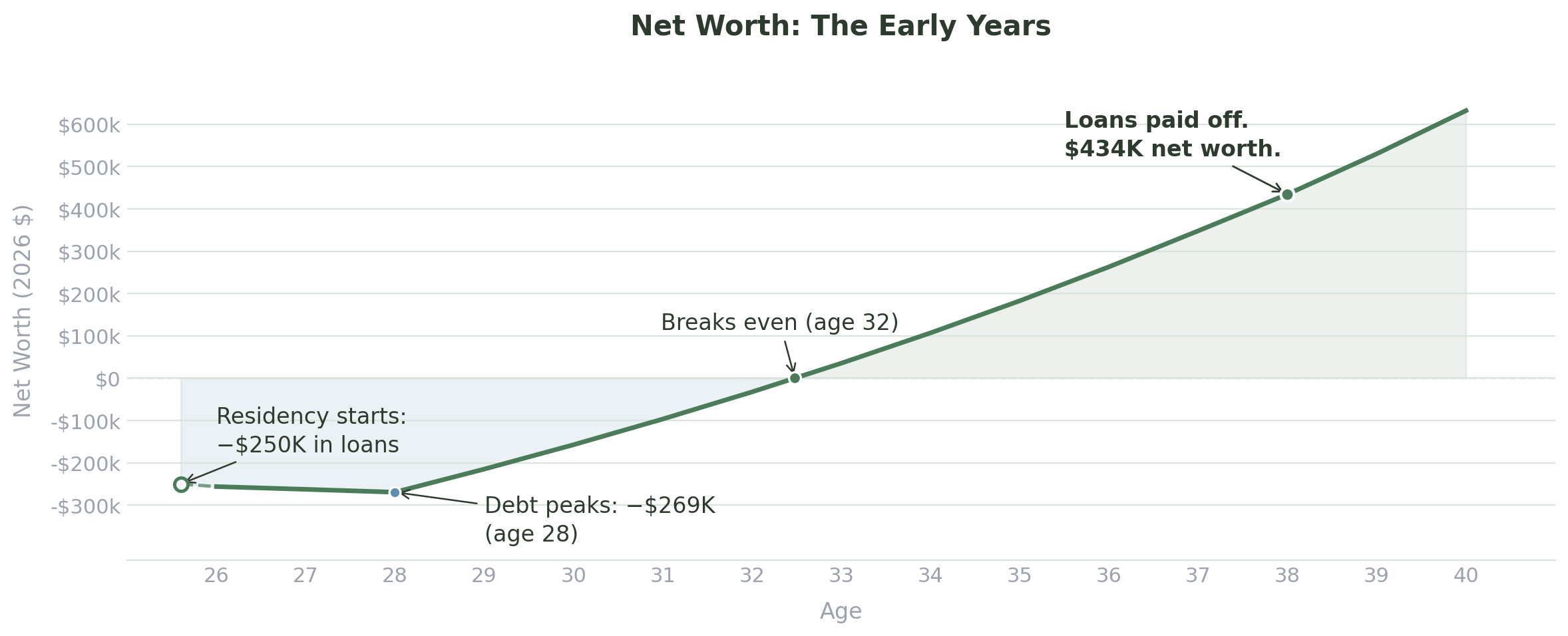

Meet Blake. Blake starts internal medicine residency at 26 with $250,000 in student loans at a 7% interest rate and, due to their modest salary, makes income driven student loan payments. By the time Blake finishes residency three years later, their student loan balance has grown to $270,000. Blake becomes an attending at 29, earning $260,000 a year but staring down the massive student loan debt.

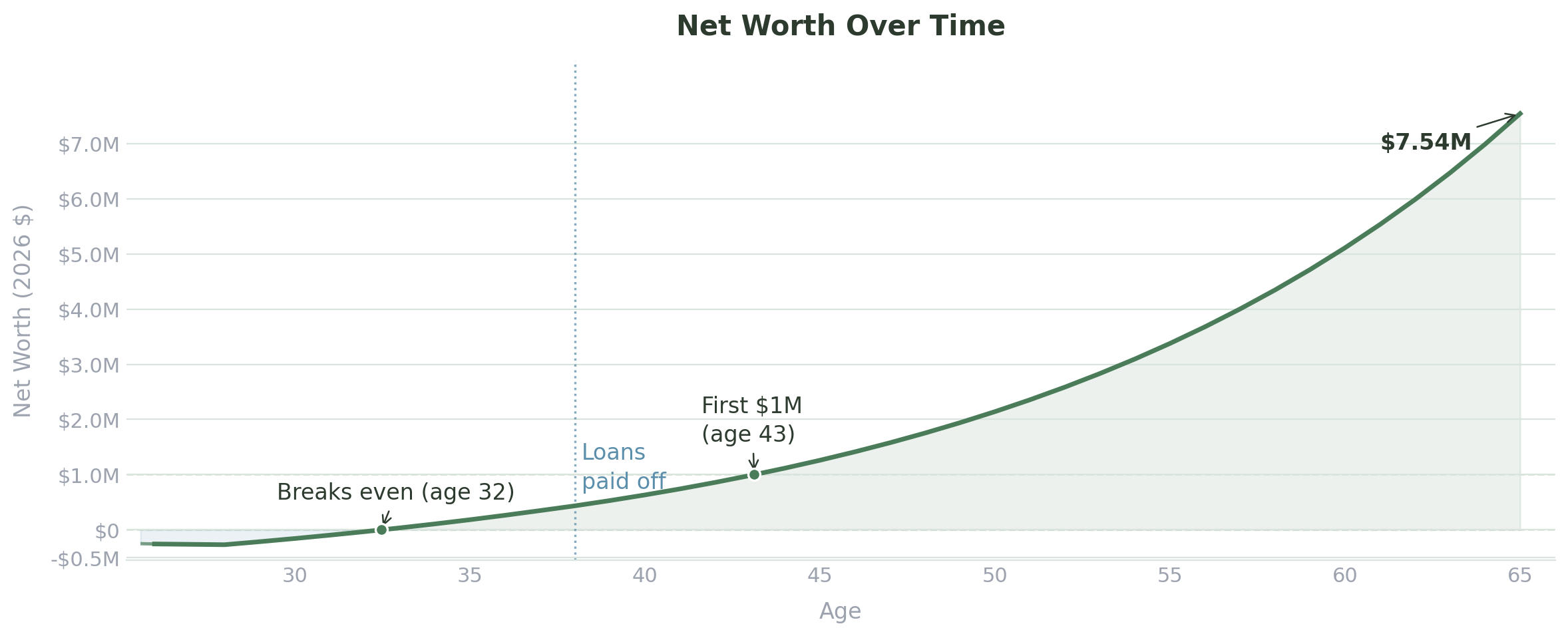

Blake retires at 65 with $7.5 million.

In spite of a brutal student loan balance, Blake gets there through one thing: diligent investing habits starting the moment the attending salary arrives. Let's talk about how.

Meet Blake

Similar to Alex, Blake commits to putting 25% of their income towards loan payments and investing. However, for Blake, this 25% has to both pay off far more loans and has less time for investments to compound.

Blake enters residency with $250,000 in student loans, which is around average for a medical school graduate. Blake's residency salary of $70,000 only allows for income driven student loan payments of $300 a month. This doesn't allow room for investing, and that's ok! Blake just needs to get through the difficulties of residency until becoming an attending, at which point they have far more flexibility.

As an attending earning $260,000, their financial picture changes dramatically: they now have the ability to make significant payments towards their loans while investing for the future.

Starting in the Red

Even though Blake is now making $260,000, the early years of being an attending are still stressful financially, in addition to the difficulties of transitioning to attending responsibilities. Blake is simultaneously paying down $270,000 of debt while building an investment portfolio from scratch. Progress can feel slow, but the foundation is being built.

Blake's net worth starts at -$250,000 after medical school, worsening to -$270,000 as the debt grows during residency. However, this trajectory reverses as soon as the attending salary arrives: Blake is paying off their loans and investing simultaneously.

Blake actually breaks even at 32, under five years into their attending career. After starting $270,000 in debt, this is a faster turnaround than most physicians would expect!

It's also worth noting that Blake starts investing seven years later than someone who graduates college and enters the workforce at 22. A shorter compounding window means that the early years of being an attending are incredibly important. Starting immediately, and staying consistent, matters more for Blake than almost anyone.

The Turnaround

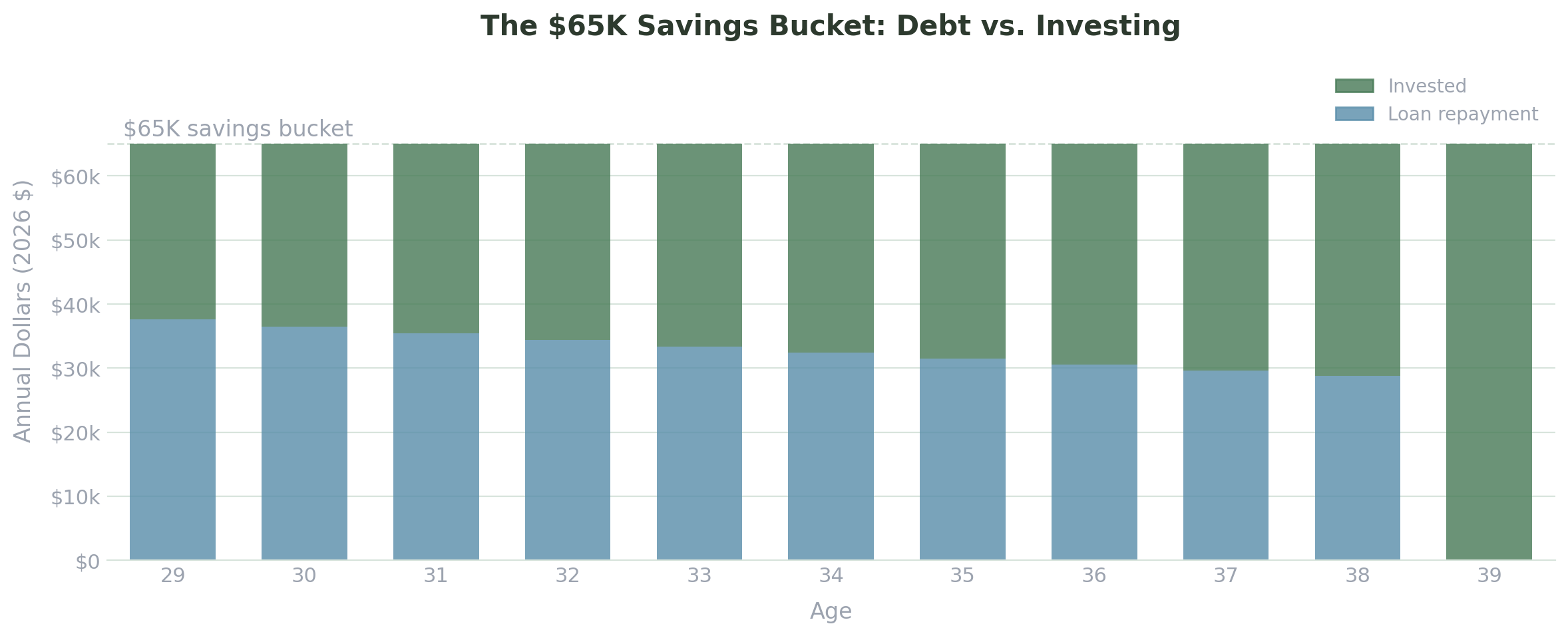

From day one as an attending, Blake's 25% savings bucket of $65,000 is doing two jobs at once.

In year one, $37,500 goes towards loan repayment while $27,500 is invested. Even though Blake is stressed about paying off their large loan balance, they invest at the same time! The debt is shrinking while the portfolio grows year over year.

Over time, the loan payments become a smaller burden as inflation erodes their real value, allowing Blake to invest slightly more money each year even while in debt. By 38, Blake has fully paid off their student loans.

At 39, Blake is able to devote the entire $65,000 to investing for the first time. After 10 years of disciplined debt repayment, Blake's portfolio takes over.

The Payoff

At 65, Blake's portfolio is worth $7,500,000 in today's dollars. Even after graduating medical school with $250,000 of loans, Blake is able to reach a net worth around the top 2% of the US due to consistent investing habits as soon as they become an attending.

Blake becomes a millionaire at 43, just 14 years after completing residency. From there, the portfolio grows faster than ever, with both compounding and Blake's continued contributions working together.

Let's put this in perspective. Blake earned a primary care salary (modest by physician standards), had $270,000 of student loan debt at the end of residency, and started investing 7 years later than a typical college graduate. And still, the outcome is exceptional.

It's worth noting that this is a relatively conservative model for a physician. Blake has no employer 401k match, no partner income, and excludes debt payoff options such as Public Service Loan Forgiveness, which can be very valuable for physicians at nonprofit or academic institutions.

The debt that felt so heavy during medical school, residency, and early attending years? By 65, it's a footnote.

Want to model your own numbers? Feel free to use my investment return calculator.

Blake doesn't use a financial advisor, which is intentional. The next post breaks down what a typical advisor arrangement actually costs over a career like Blake's. The number might surprise you.

And if you want to build a financial plan that accounts for your specific training path and goals, that's what my 1:1 coaching program is for. Feel free to reach out and set up a free consultation.

Get notified when new posts go live.