Your Financial Advisor Is Charging You Millions

June 2, 2026

Most people who work with a financial advisor don't understand what they're actually paying. The vast majority of financial advisors charge AUM ("assets under management") fees, which are deducted directly from your portfolio each year, not billed as an invoice. There's no line item, no annual statement that says "you paid $8,000 in fees this year." Instead, the money just quietly disappears. There's a reason that financial advisors hide these costs.

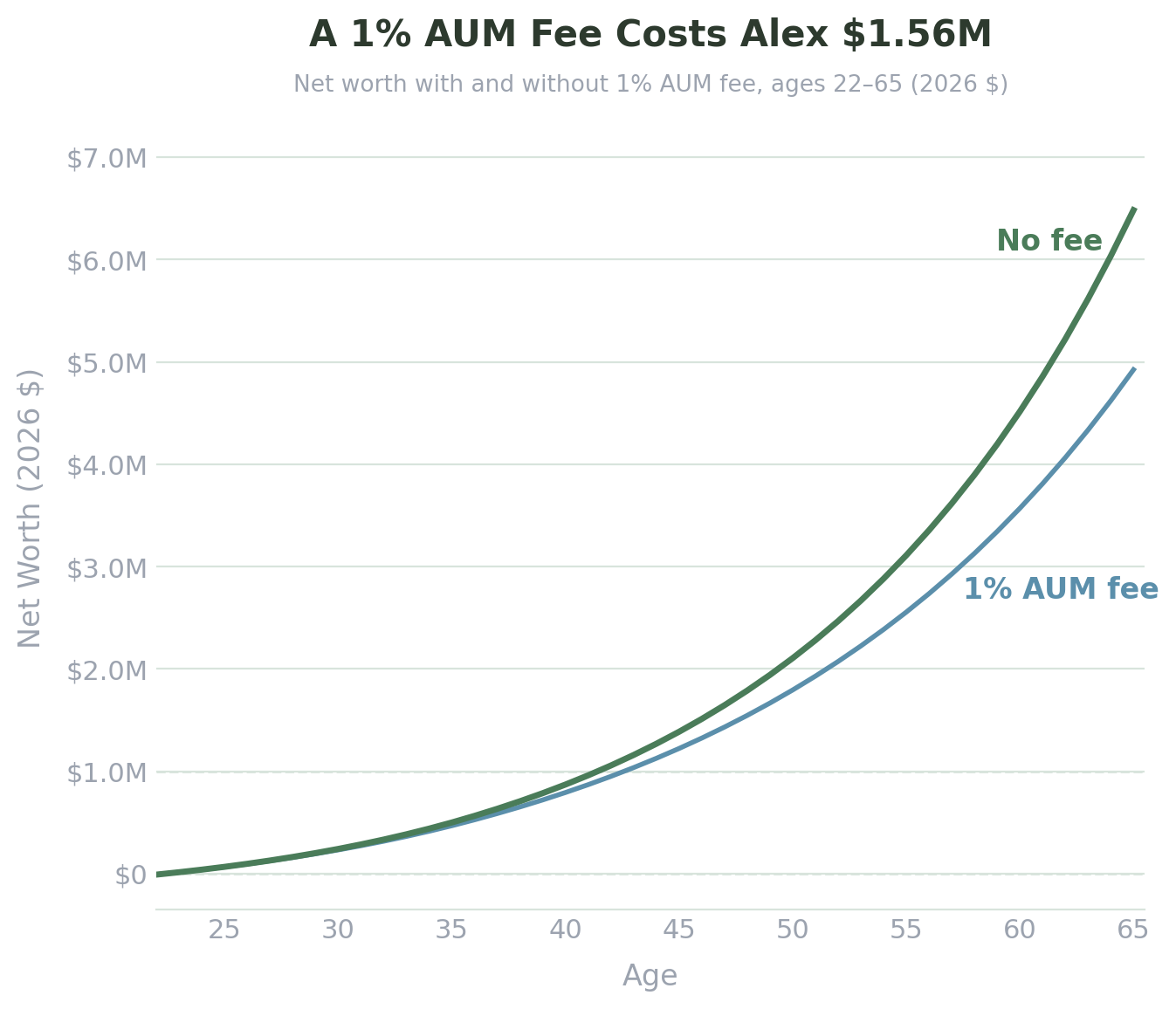

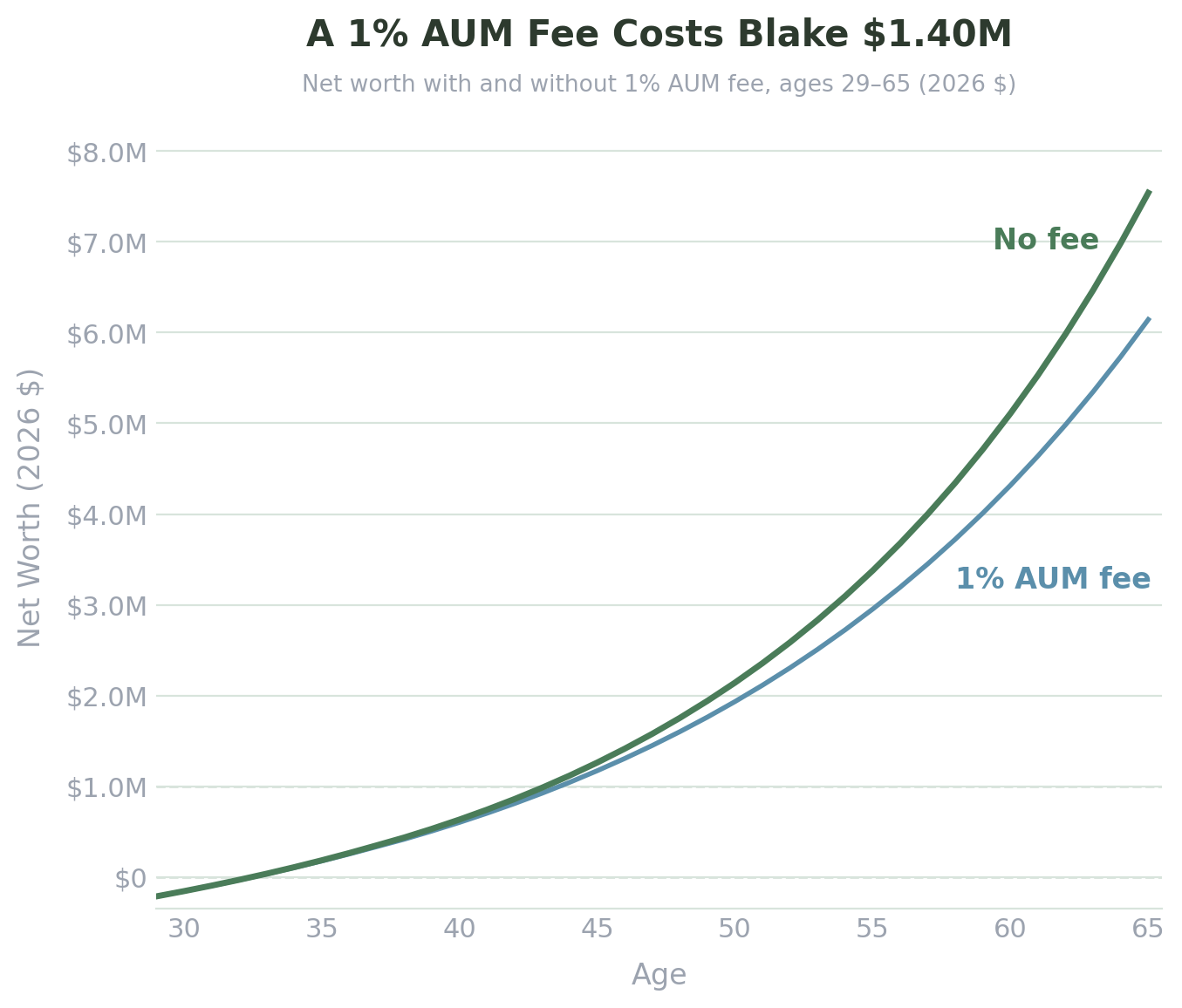

Consider two high earners: a tech worker and a physician, both consistent investors throughout their careers. A standard 1% AUM fee costs the tech worker $1.56 million by retirement. The physician loses $1.40 million. Same habits, same discipline, same everything… except a fee most clients don't fully understand before they sign.

Millions In Fees

The charts below show the investing trajectories for the tech worker (Alex) and physician (Blake) outlined in previous posts, with one addition: a 1% AUM fee charged every year.

Early in both careers, the fee is nearly invisible. At 30, Alex has lost about $13,000 to fees, barely noticeable against a growing portfolio. However, the fee compounds just like the portfolio does, and by retirement the gap is well over a million dollars for both.

To put this in perspective, Alex loses more to fees than they earn in their first 17 years of working. Blake loses more than 5 years of their attending salary. These are massive, life changing amounts of money, quietly extracted from your portfolio year after year. Most clients never see these numbers. Financial advisors don't put them in front of you.

Compounding Works Both Ways

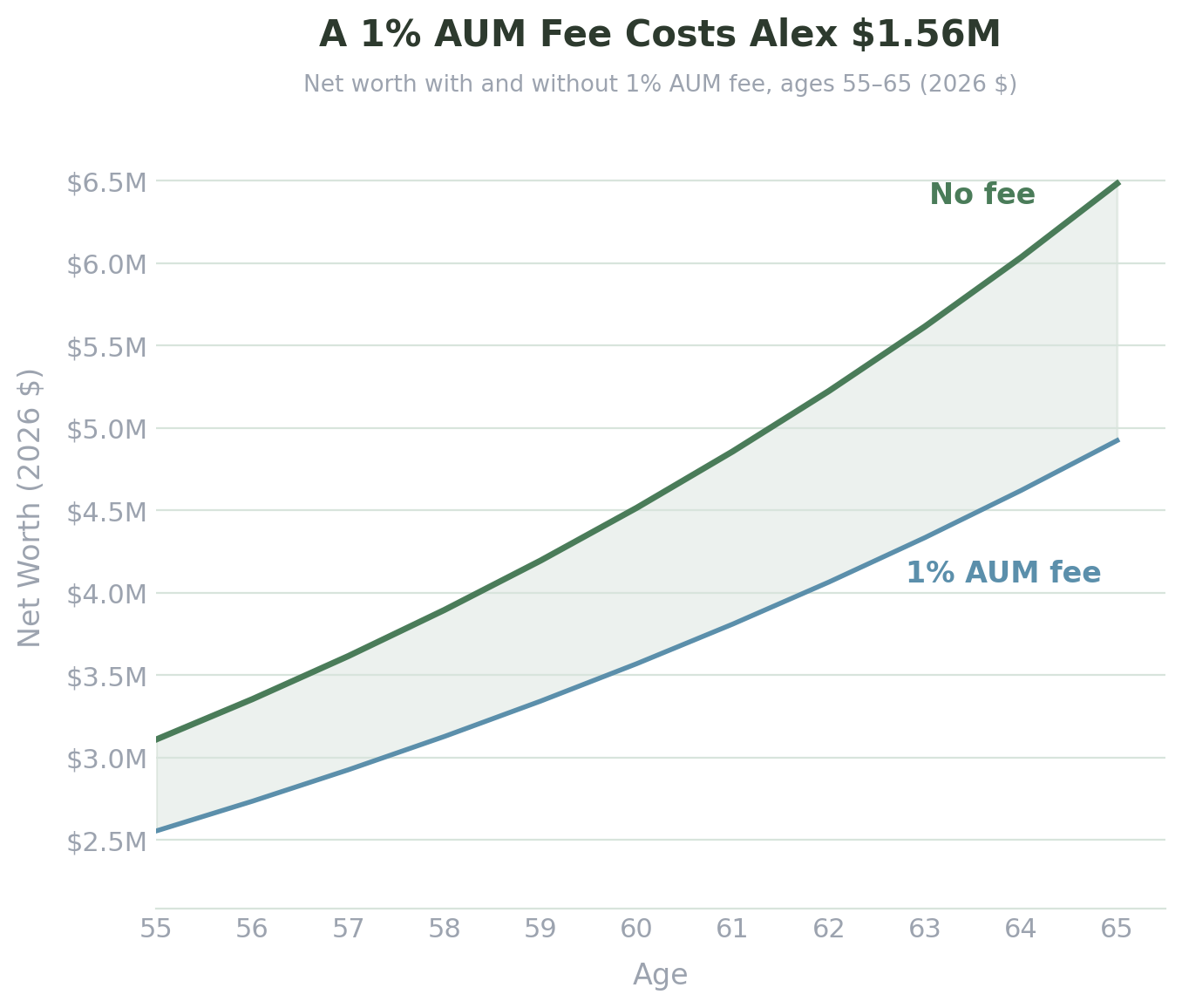

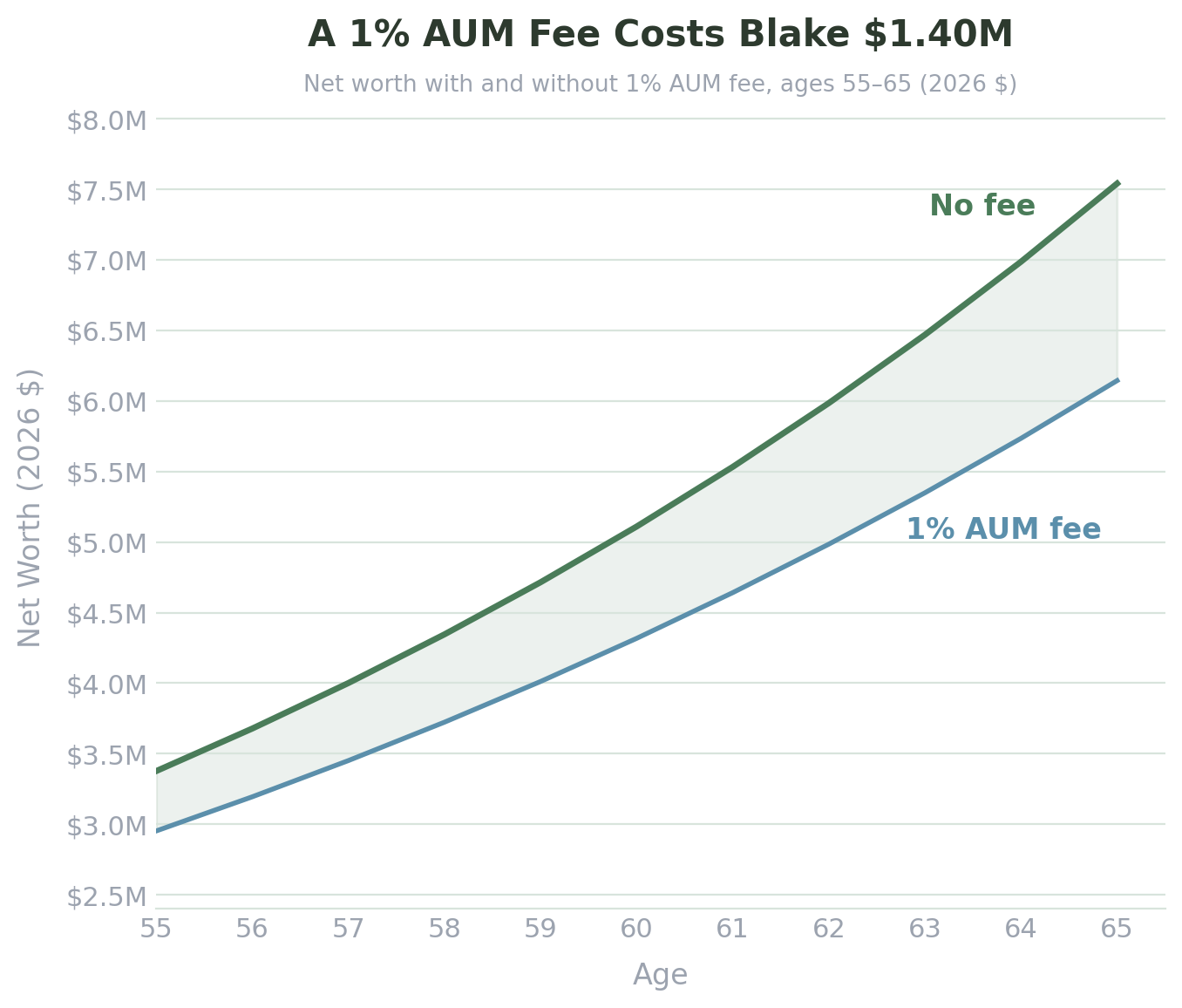

The charts below zoom into the final decade of both careers, where the fee damage is most visible.

The reason the gap is so large comes down to compounding. In the previous posts on Alex and Blake, we got to see the power of long term compounding for creating wealth over the course of a career. The fees compound against you in just as powerful a fashion. A 1% fee on your portfolio doesn't just cost you 1% that year, but that money also can't keep compounding for you. A dollar taken in fees at 35 doesn't just cost a dollar! It costs a dollar plus 30 years of investing returns on that dollar.

This is why the losses accelerate over time. As your portfolio grows, the fees get bigger, and those losses compound against you even more. In the final decade alone, Alex loses $900,000 to fees and Blake loses $650,000.

Alex actually loses $160,000 more to fees than Blake, despite earning a lower salary throughout their career. Blake's compressed compounding window slightly limits the fee's damage, as there are fewer years for it to compound.

The Confidence You're Not Building

The financial losses from AUM fees are huge, but they aren't even the only cost.

Many physicians and high earners hand their finances over to an advisor and feel relieved to have someone else dealing with it. However, an advisor managing your portfolio doesn't teach you how to manage your own money. Most financial anxiety lives in the day to day questions: am I spending too much this month? Does this big purchase fit my plan? Am I saving enough? Learning to manage your finances yourself gives you the tools to answer these questions with confidence. No advisor can build that confidence for you.

People who understand their own finances experience a more durable kind of financial confidence. Understanding your own finances gives you the security of knowing where you stand.

Paying More, Getting Less

The fee calculations above assume that a financial advisor at least matches the market. Most don't.

According to S&P's SPIVA scorecard, 94% of actively managed funds underperformed the market over the past 20 years. Over a 15-year period, there was not a single fund category where the majority of active managers beat their benchmark. The losses shown above are actually conservative estimates.

This helps explain something you may have noticed in an advisor-managed portfolio: the complexity. Dozens of funds, overlapping positions, elaborate allocations. A simple index fund portfolio would outperform the vast majority of these arrangements over the long run, at a fraction of the cost. The complexity exists to justify the fee, not to generate better returns.

The AUM model has a structural incentive problem. An advisor's revenue grows as your portfolio grows, regardless of the value of their advice that year. The incentives are clear: the longer you stay, the more they make, regardless of what that costs you.

For most high earners, the answer is simpler than the financial industry wants you to believe: low-cost index funds, consistent contributions, and an understanding of your own finances.

Ready to stop wondering whether you're spending too much, saving enough, or actually on track? That's exactly what my 1:1 coaching program is built for. Feel free to reach out and set up a free consultation.

Get notified when new posts go live.